June 2026

Here comes the sun!

June is here and summer has begun. Summer is my favorite season. Talking to my grandson earlier today I remember why. I asked him if school ends this week and he was so excited. I asked why and he said he gets to play every day and go to the pool for swimming lessons. When I was 7 I felt the same way. Summer holidays were the best. While our kids look forward to time off for a long summer, the economy is heating up.

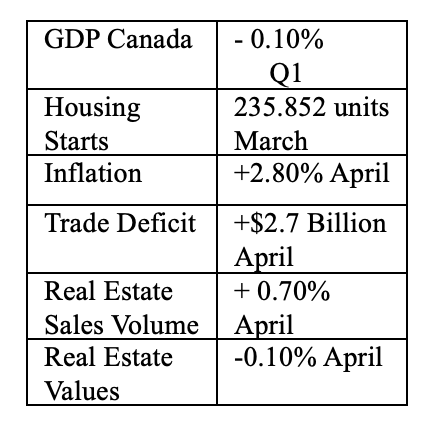

Bank of Canada held the rate at 2.25% where it has been since last October. Canada is in a “technical” recession and the media and many economists think it is not in a “real” recession. Our trade surplus grew last month mainly due to the high price of oil resulting form the middle east conflict. Inflation also rose to 2.8% in April and is expected to stay elevated and that is why the Bank of Canada did not drop the rate despite a technical recession.

The dispute about whether we are in a real recession or not can be explained by the K-shaped economy which I explained in a previous newsletter and I will explain in my June blog. In a K-shaped economy the wealthy thrive and don’t experience economic setbacks or recessions whereas the middle to lower class has a hard time making ends meet and feel a constant recession like economy. I think the K-shaped economy is taking hold in Canada and other countries and that is why the wealthy don’t feel it but the average Canadian feels it intensely.

When listening to a large US wealth management CEO last week, he said that the biggest phenomena in the US economy currently is too many dollars chasing investments. In the mortgage industry we too are finding investment returns being pressured to the downside due to large volume lenders cutting pricing. One large MIC last week advertised first mortgage rates to 75% at 5.49%. A bank five-year term currently carries a rate only a point lower. I have never seen the private mortgage market pricing so close to bank rates. Systemic large increases in the money supply can be a harbinger of a bubble coming to the economy if not managed properly by the policy makers.

We continue to recommend a cautious approach to investments in this turbulent time. GIC rates are 3.65% for one year and we can get clients a rate enhancement for amounts over $500,000.00 Also MIC shares provide good protection in a diversified mortgage pool of funds and the returns are double that of a GIC. Call or email us for more information.

Monthly Quiz

Here is a fun quiz for the start of Summer. I scored 50%. See how you do: Summer Quiz

Financial Literacy

How to Prepare Consumer Finances for Summer

To prepare consumer finances for summer, consider the following tips:

1. Review your expenses: Assess your current financial situation and track your spending to ensure you are making the most of your money.

2. Plan ahead: Prioritize your expenses and create a budget for each month throughout the summer to avoid overspending.

3. Use cash, not credit: Decide on a set amount of cash that you feel comfortable spending each week to encourage spending and avoid unnecessary credit card charges.

4. Cut back on non-essentials: Identify and cut back on non-essential expenses to have money for things you need or really want.

5. Check for unused contribution room: Review your retirement accounts to ensure you are maximizing your contributions and not missing out on any unused contribution room. With kids and grandkids going back to school in the fall be sure to plan to maximize their RESP.

By following these tips, you can enjoy the summer without overspending or sacrificing fun.